THE STOCK AND BOND MARKETS HAVE HAD SPECTACULAR RETURNS SINCE THE TROUGH OF THE MARKET ON CHRISTMAS EVE 2018.

The stock market (S&P 500) is now up 44.7% and the bond market (Bloomberg Barclays US Aggregate Bond Index) is up 9.6%. While investors have no doubt enjoyed these returns, they should be aware of the potential for an unintended, and potentially unwanted, consequence of strong markets.

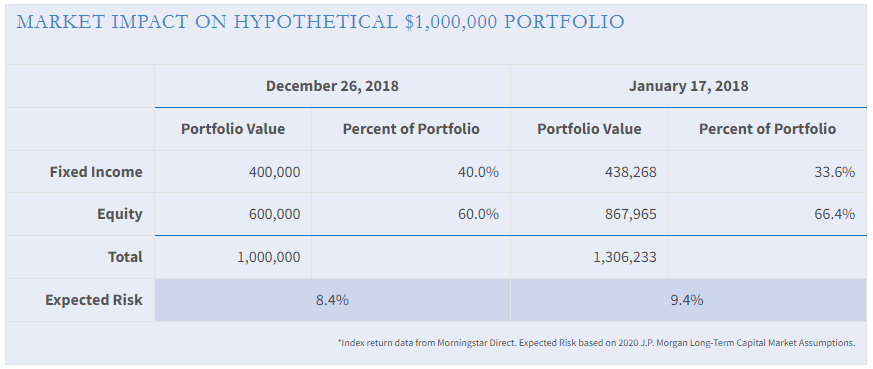

The high levels of returns can dramatically change the asset allocation of a portfolio, and, in this case, add significant equity risk. For example, a simple two asset portfolio that was 60% large cap US stocks and 40% US bonds on December 24, 2018, would have become 66.4% equity and 33.6% fixed income if the investor had reinvested dividends and not made any other trades in the portfolio. Based on the 2020 J.P. Morgan Long-Term Capital Market Assumptions:

The original portfolio had an expected standard deviation (risk) of 8.4% and the current portfolio has a standard deviation of 9.4%. As a result, the market moves have added 11.9% more risk to your portfolio.

READJUST TO TARGET ALLOCATIONS QUARTERLY

At Fairman Financial, we recommend investors rebalance their portfolio back toward the original allocation target at least quarterly, or more often if market movements have created a significant deviance from the target. Morningstar research has shown that rebalanced portfolios have better risk adjusted returns than un-rebalanced portfolios, but that there is no conclusive evidence as to the most optimal rebalancing schedule. The rebalancing process:

- Maintains the targeted risk profile of the portfolio

- Is a systematic methodology that generally buys low and sells high

- Provides discipline to the investment process

- Has the potential for reduced portfolio drawdowns

Rebalancing a two asset portfolio for a non-taxable investor is a relatively simple process, but the more realistic scenario of a diversified investor that has taxable, tax deferred, and tax free assets could add significant complexity to the rebalancing process. The investor will have to balance the potential of a taxable capital gain versus the benefit of maintaining the portfolio’s asset allocation closer to the target. There may be other complicating factors such as the need to replace a manager or strategy, required minimum distributions from an IRA, and needs for client liquidity.

Ultimately, rebalancing can feel like a puzzle where getting all of the pieces into place requires a combination of both art and science to account for multiple competing factors. It can; however, be an important contributor to an investor achieving and maintaining the balance between risk and reward that they desire.